Market Power I

Adam Smith

1723-1790

"People of the same trade seldom meet together, even for merriment and diversion, but the conversation ends in a conspiracy against the public, or in some contrivance to raise prices, (Book I, Chapter 2.2)"

Smith, Adam, 1776, An Enquiry into the Nature and Causes of the Wealth of Nations

Market Power

All sellers would like to raise prices and extract more revenue from consumers

Competition from other sellers drives prices down to match MC(q) (and bids costs and rents upwards to match prices)

If a firm in a competitive market raised p>MC(q), would lose all of its customers

A firm with market power has the ability to raise price above its marginal cost and not lose all of its customers

Monopoly

- We start with a simple model of monopoly: a market with a single seller

Firm's products may have few close substitutes

Barriers to entry, making entry costly

Firm is a "price-searcher": can set optimal price p∗ in addition to quantity q∗

- Must search for (q∗,p∗) that maximizes π

The Monopolist's Problem I

- The monopolist's profit maximization problem:

Choose: < output and price: (qo,po)>

In order to maximize: < profits: π>

The Monopolist's Problem II

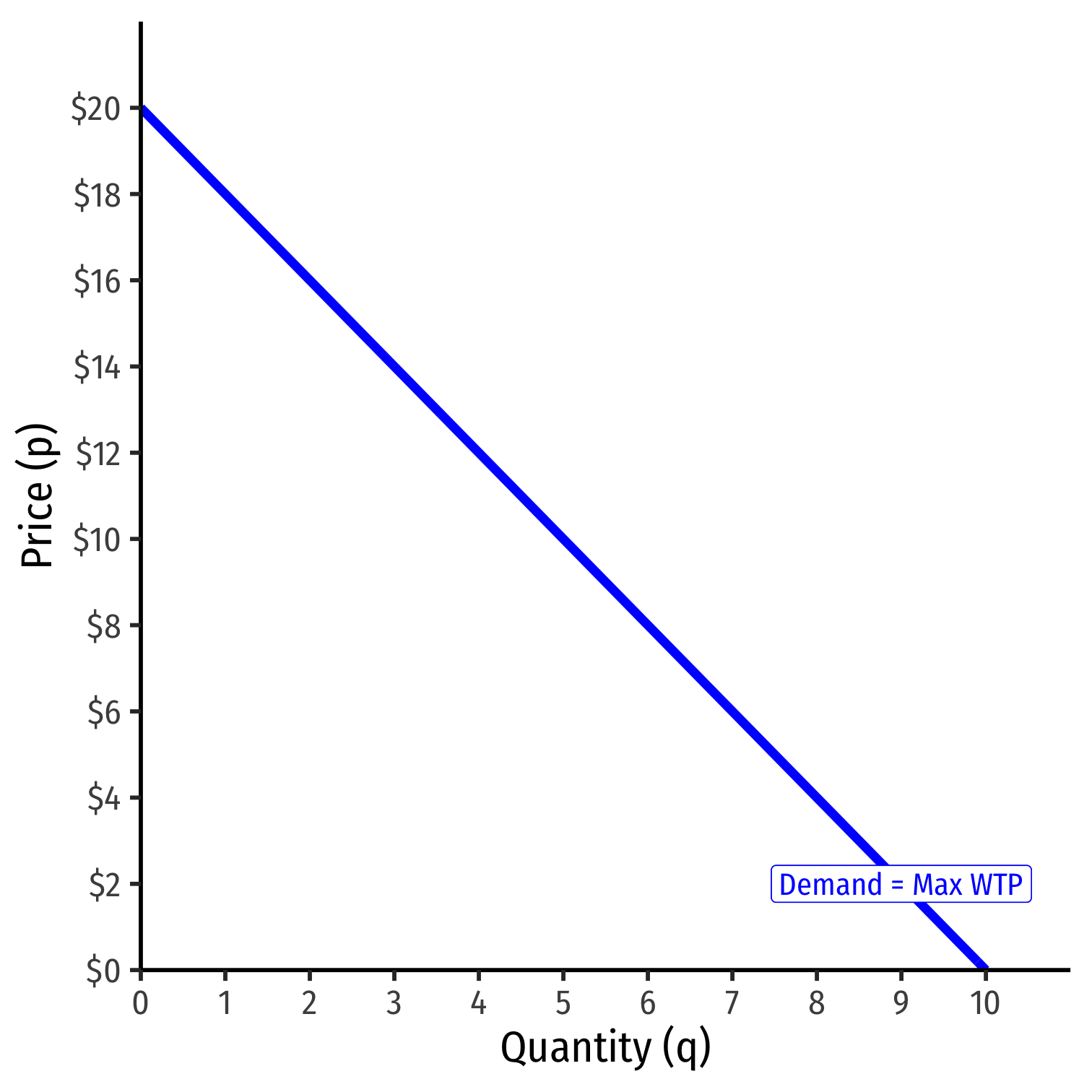

Monopolist is constrained by relationship between quantity and price that consumers are willing to pay

Market (inverse) demand describes maximum price consumers are willing to pay for a given quantity

Implications:

- Monopolies can't set a price "as high as it wants"

- Monopolies can still earn losses (and exit in the long run)

The Monopolist's Problem II

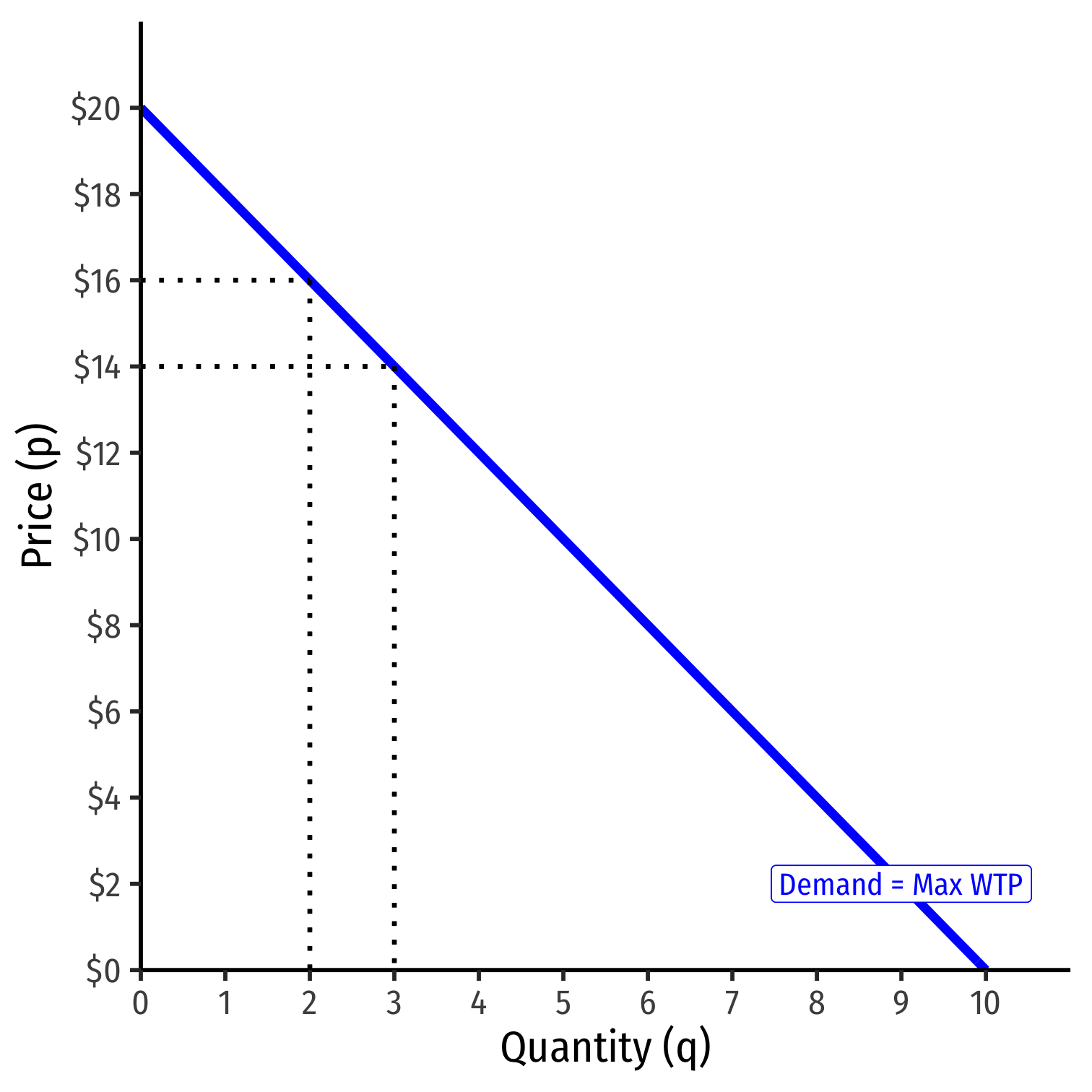

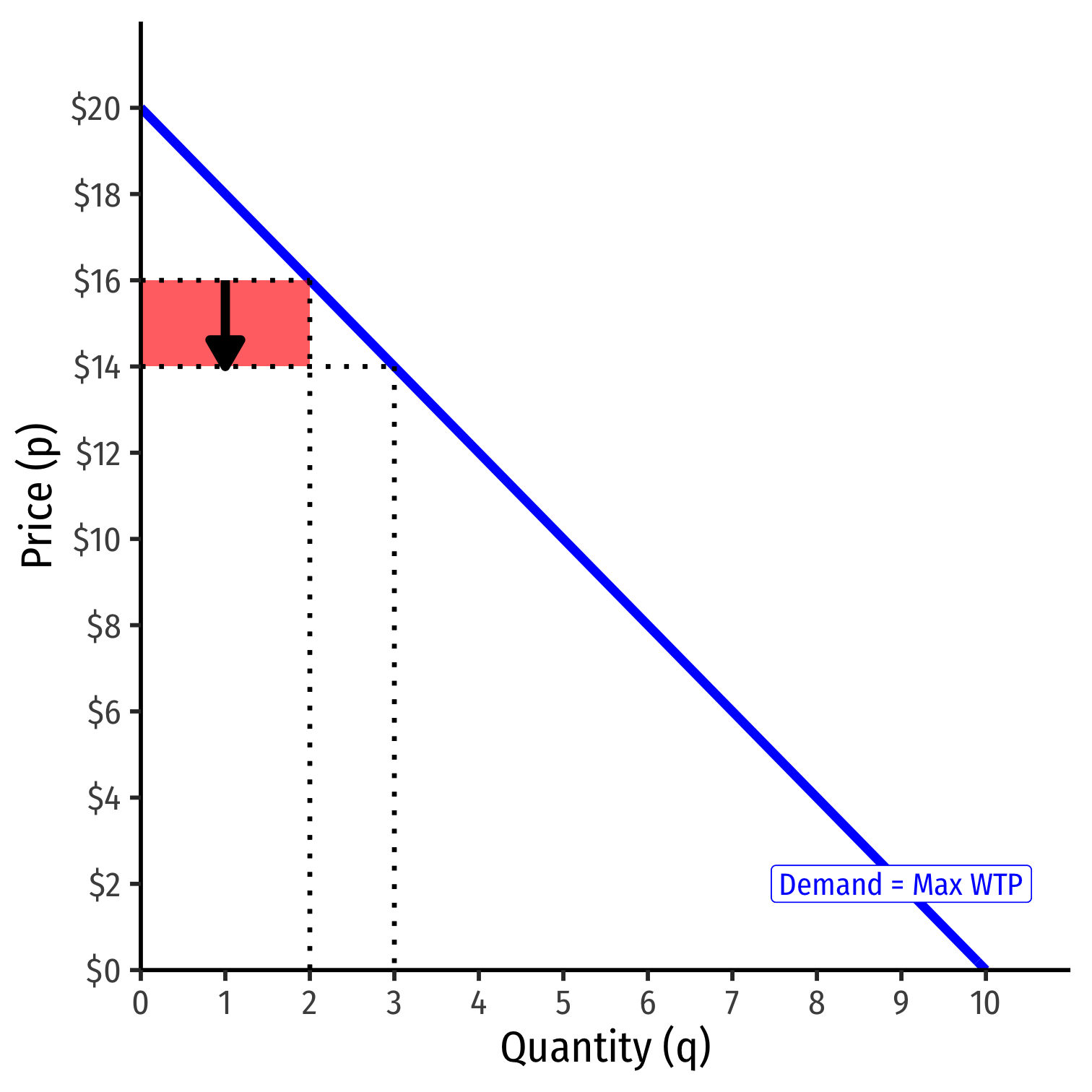

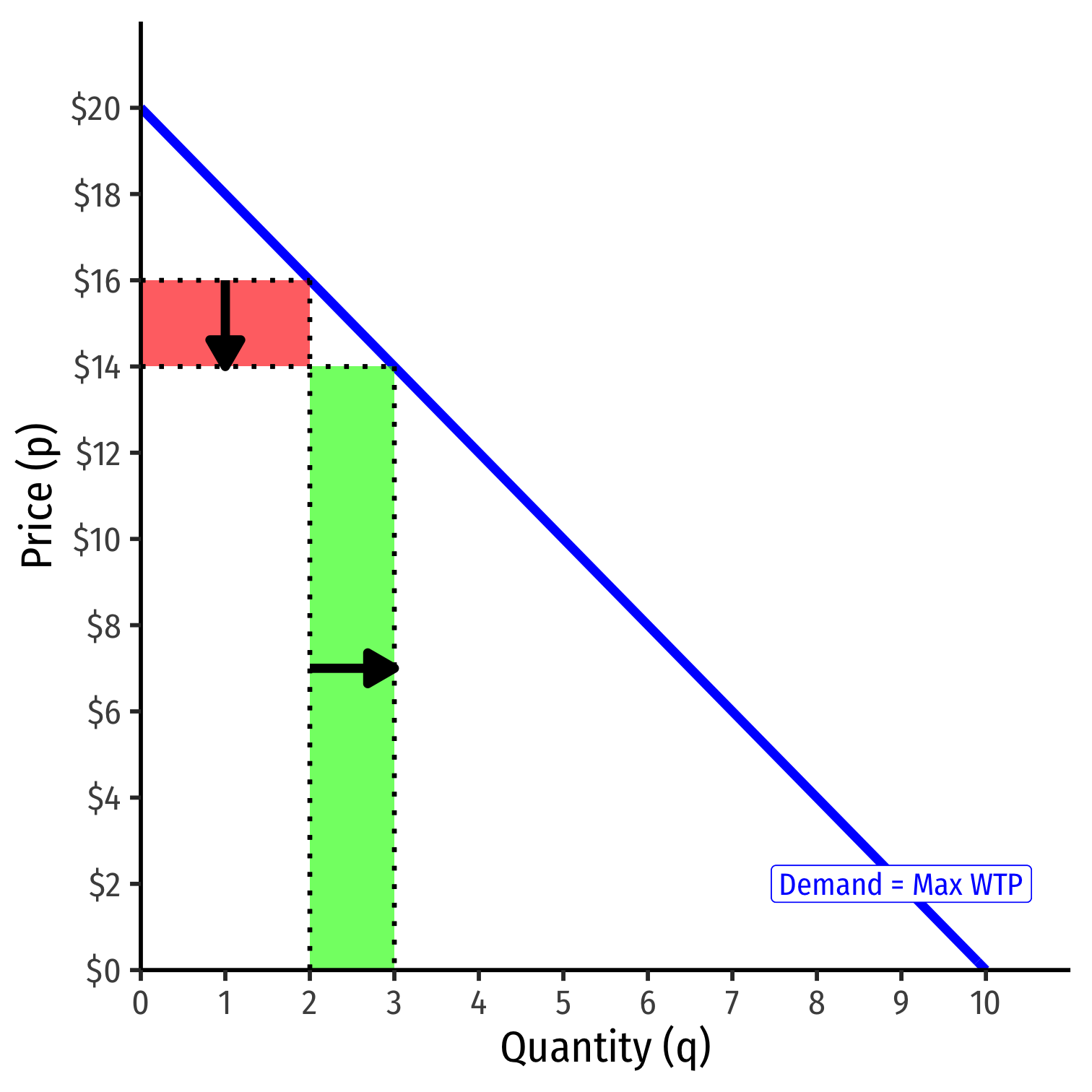

- As monopolist chooses to produce more q∗, must lower the price on all units to sell them

The Monopolist's Problem II

As monopolist chooses to produce more q∗, must lower the price on all units to sell them

Price effect: lost revenue from lowering price on all sales

The Monopolist's Problem II

As monopolist chooses to produce more q∗, must lower the price on all units to sell them

Price effect: lost revenue from lowering price on all sales

Output effect: gained revenue from increase in sales

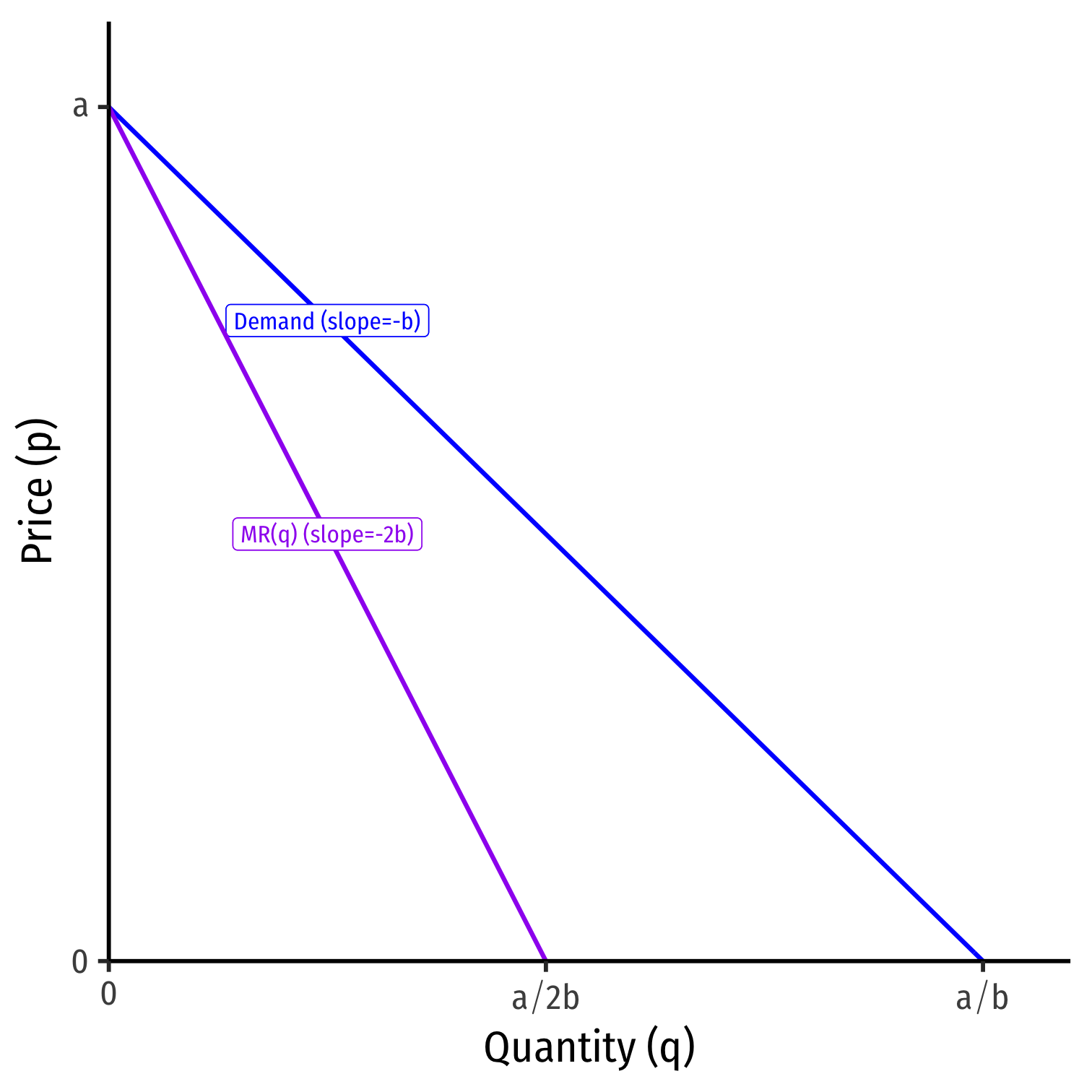

Monopoly and Revenues III

p(q)=a−bqMR(q)=a−2bq

- Marginal revenue starts at same intercept as Demand (a) with twice the slope (2b)

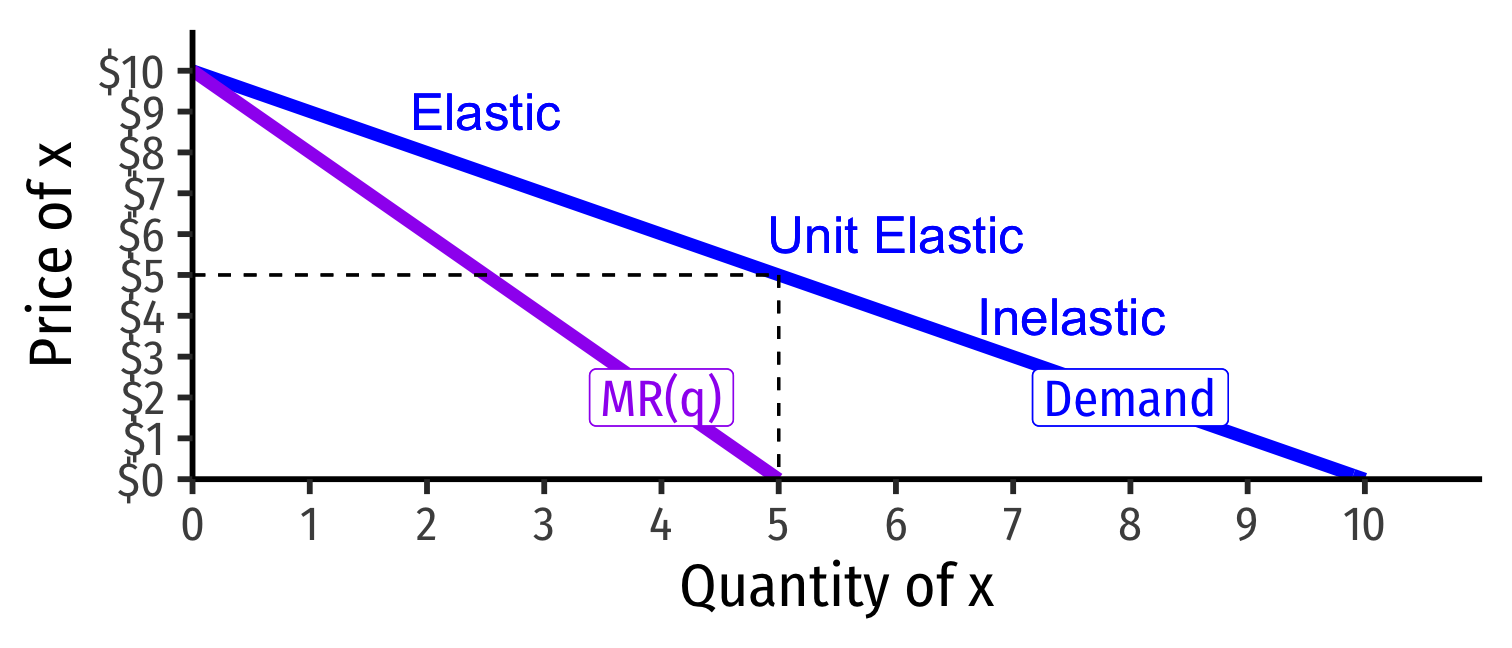

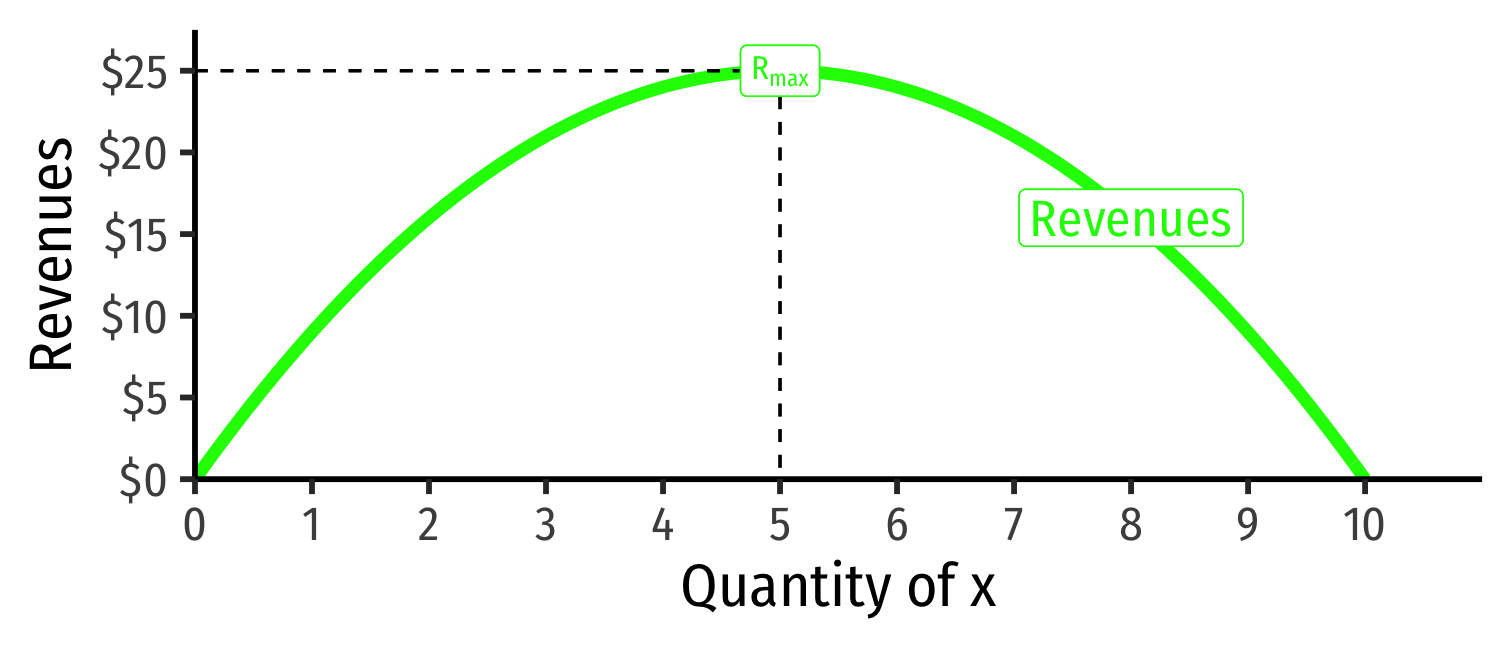

Revenues and Price Elasticity of Demand II

- Here is finally further evidence for pthe relationship we showed in lesson 1.9

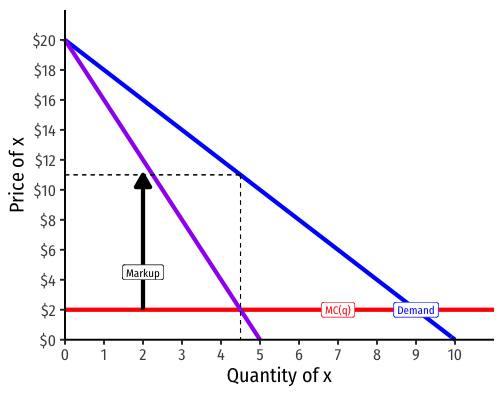

Measuring Markup Prices

- How much does a monopolist mark up price over cost?

Measuring Markup Prices

- How much does a monopolist mark up price over cost?

MR(q)=MC(q)

Measuring Markup Prices

- How much does a monopolist mark up price over cost?

MR(q)=MC(q)p(1+1ϵ)=MC(q)

Measuring Markup Prices

- How much does a monopolist mark up price over cost?

MR(q)=MC(q)p(1+1ϵ)=MC(q)p=MC(q)1+1ϵ

Measuring Markup Prices

p=MC(q)1+1ϵ

Perfect competition: p=MC(q) (allocatively efficient)

Monopolists mark up price above MC(q)

Size of markup depends on price elasticity of demand

- ↓ price elasticity: ↑ markup

- i.e. the less responsive to prices consumers are, the higher the monopolist can charge

The Lerner Index I

- Lerner Index measures market power as % of firm's price that is markup above (marginal) cost

L=p−MC(q)p=−1ϵ

- L=0⟹ perfect competition

- (since P=MC)

- As L→1⟹ more market power

The Lerner Index II

The more (less) elastic a good, the less (more) the optimal markup: L=p−MC(q)p=−1ϵ

"Inelastic" Demand Curve

"Elastic" Demand Curve

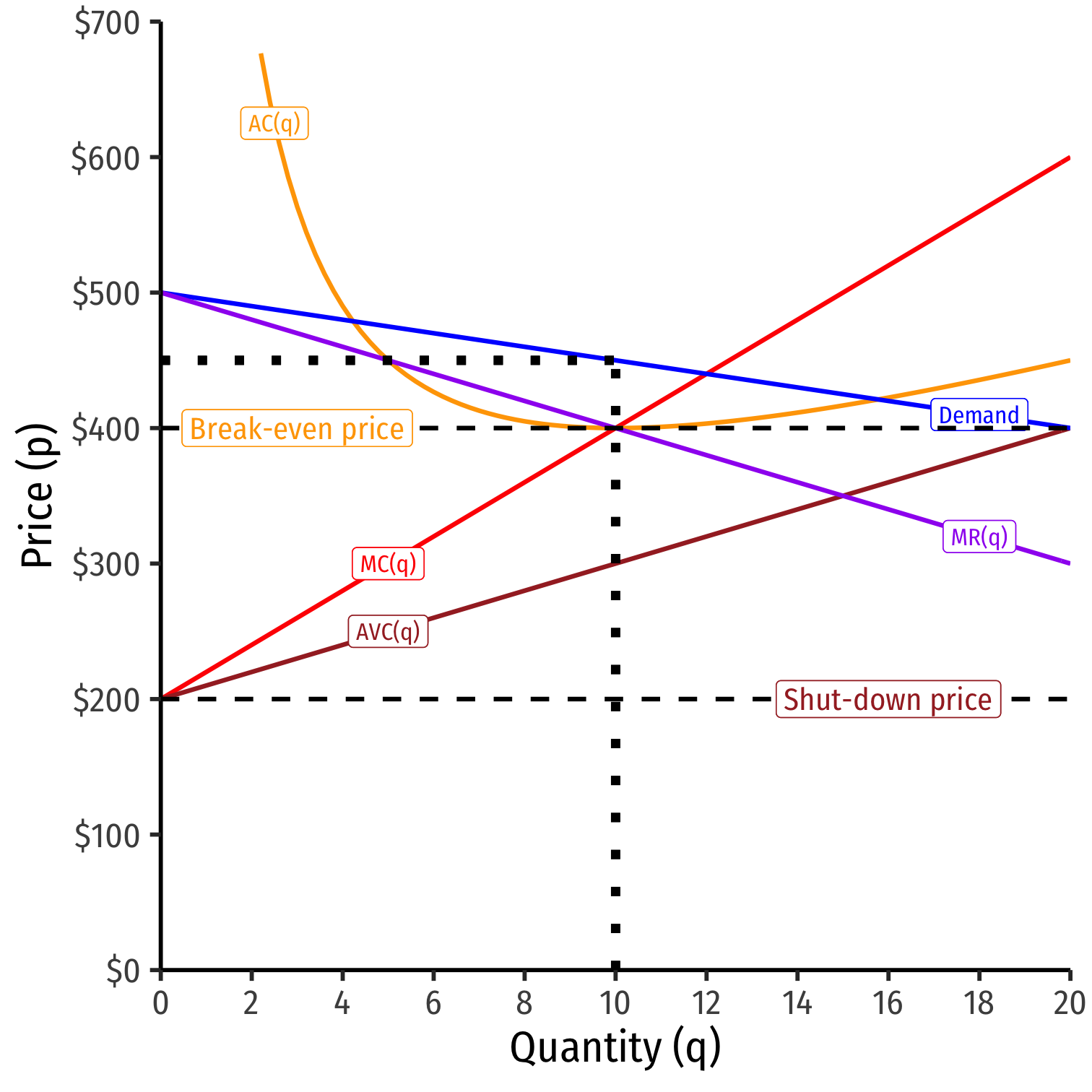

Profit-Maximizing Price and Quantity (Graph)

- Profit-maximizing quantity is always q∗ where MR(q) = MC(q)

Profit-Maximizing Price and Quantity (Graph)

Profit-maximizing quantity is always q∗ where MR(q) = MC(q)

But monopolist faces entire market demand

- Can charge as high as consumers are WTP

Profit-Maximizing Price and Quantity (Graph)

Profit-maximizing quantity is always q∗ where MR(q) = MC(q)

But monopolist faces entire market demand

- Can charge as high as consumers are WTP

Break even price p=AC(q)min

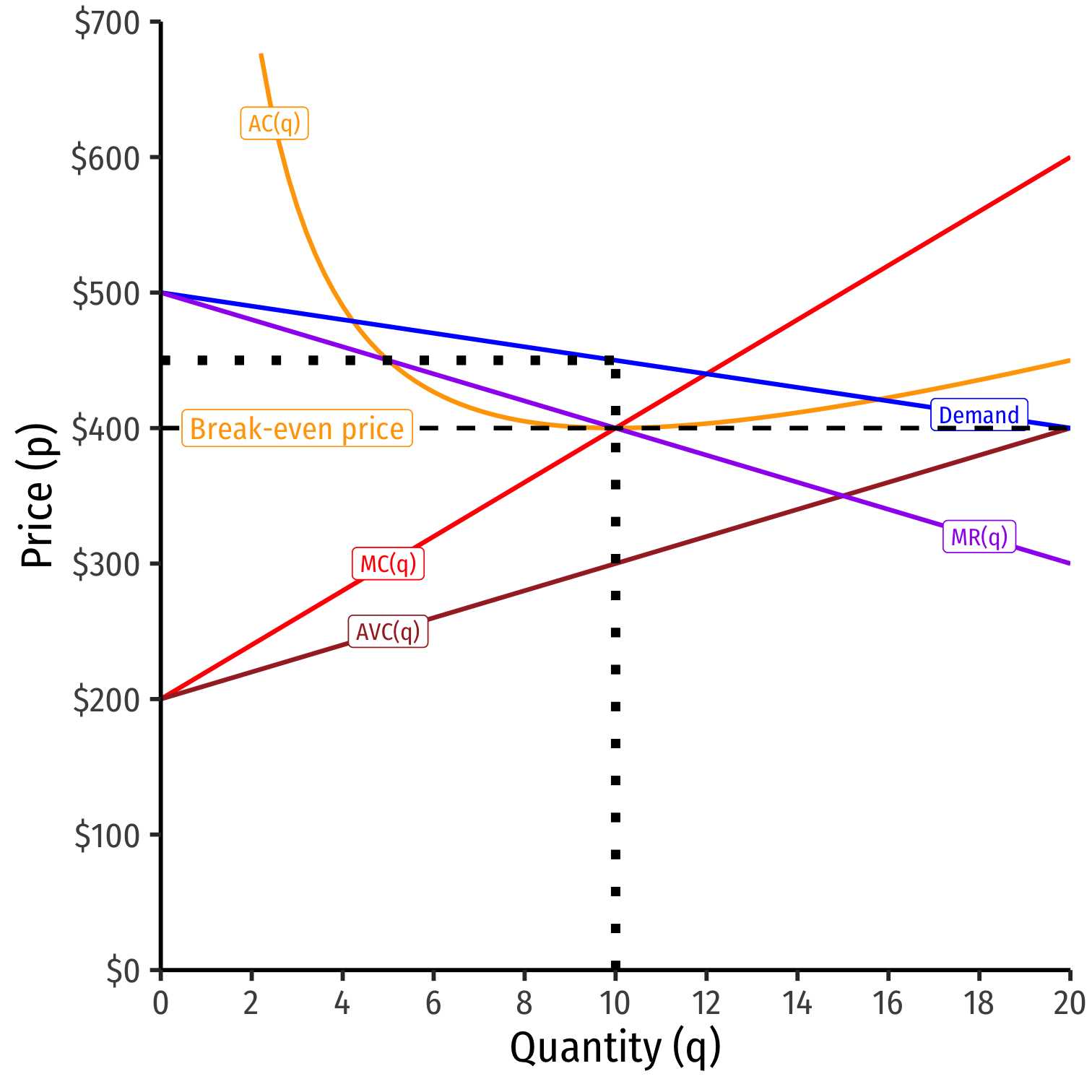

Profit-Maximizing Price and Quantity (Graph)

Profit-maximizing quantity is always q∗ where MR(q) = MC(q)

But monopolist faces entire market demand

- Can charge as high as consumers are WTP

Break even price p=AC(q)min

Shut-down price p=AVC(q)min