Returning to Firms I

Recall: firms convert some goods to other goods:

Inputs: x1,x2,⋯,xn

- Examples: worker efforts, warehouse space, electricity, loans, gasoline, cardboard, fertilizer, computers, software programs, etc

Output:1 q

- Examples: oil, cars, legal services, mobile apps, vegetables, consulting advice, financial reports, etc

Returning to Firms II

Suppose a firm sells output q at a price p

It can buy each input xi at an associated price pi

- labor l at wage rate w

- capital k at rental rate r

Profit ⟹ improving the (total) value of resources

- bought inputs at some total cost

- sold as final product at some market price

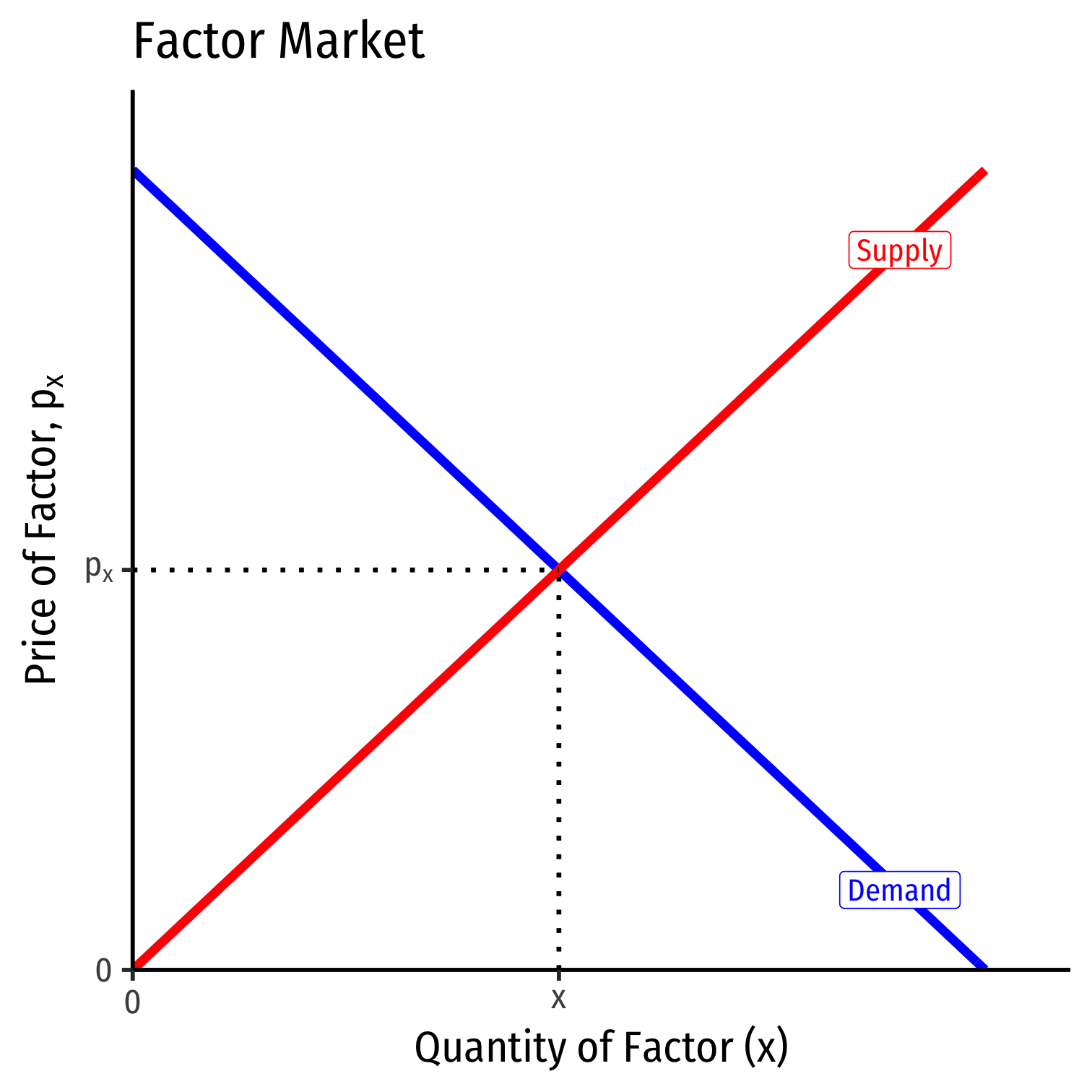

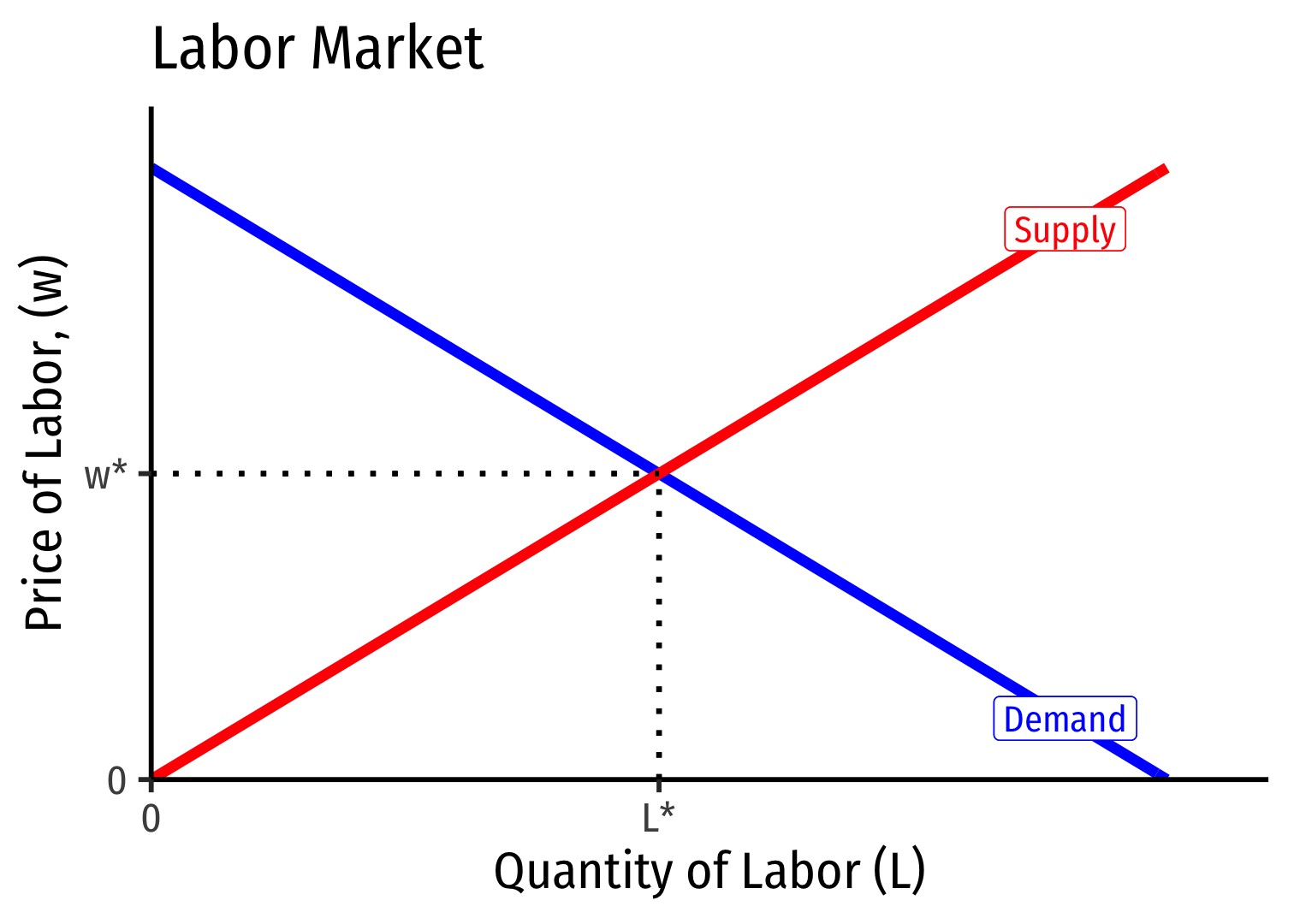

Supply and Demand in Factor Markets

The price of a factor is governed by the same market forces as output: Supply and Demand

Supply of Factor: willingness of factor owners to accept and sell/rent their services to firms

- landowners, workers, capitalists, resource owners, suppliers

Demand for Factor: willingness of firms to pay for factor services

Factor Market Prices and Opportunity Costs

In functioning factor markets, the factor price represents the opportunity cost of hiring a factor for an alternative use

- Firms not only pay for direct use of a factor, but also indirectly for not using it in an alternate process!

Example: a producer of hammers buys steel, pays (the opportunity cost) for "taking" the steel away from alternative uses

Example: e.g. salary for a skilled worker must be high enough to keep them at their current firm, and not be attracted to other firms/industries

Labor Markets

Empirically, about 70% of total cost of production comes from labor

We'll focus just on the market for labor as an example factor market

Can do the same for any factor market

- (e.g. capital, land, materials, etc.)

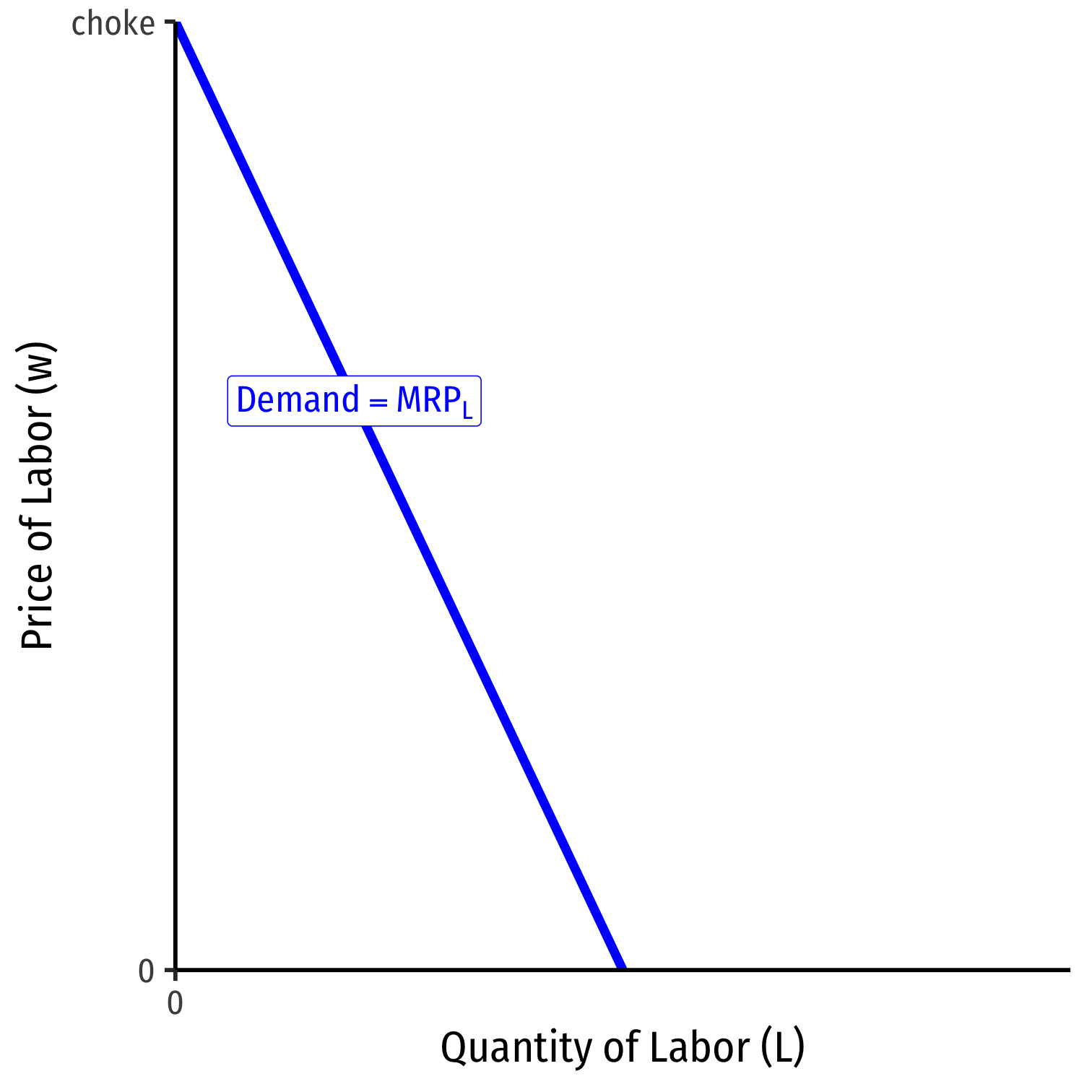

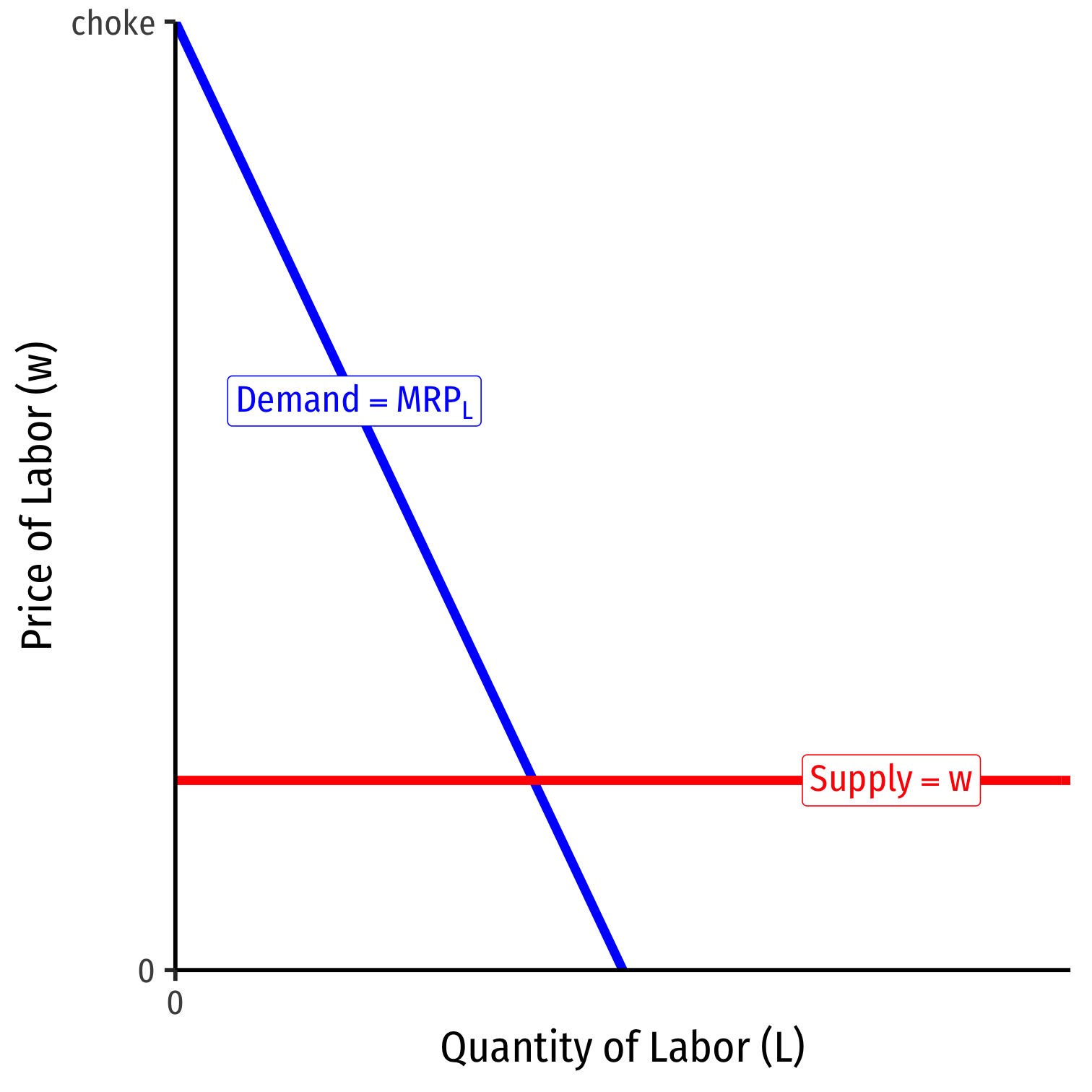

Marginal Revenue Product for Competitive Firms

MRPL=MPL∗MR(q)

- For a firm in a competitive (output) market, firm's MR(q)=p, hence

MRPL=MPL∗p

Marginal benefit of hiring labor, MRPL falls with more labor used

- production exhibits diminishing marginal returns to labor

Choke price for labor demand: price too high for firm to purchase any labor

]

]

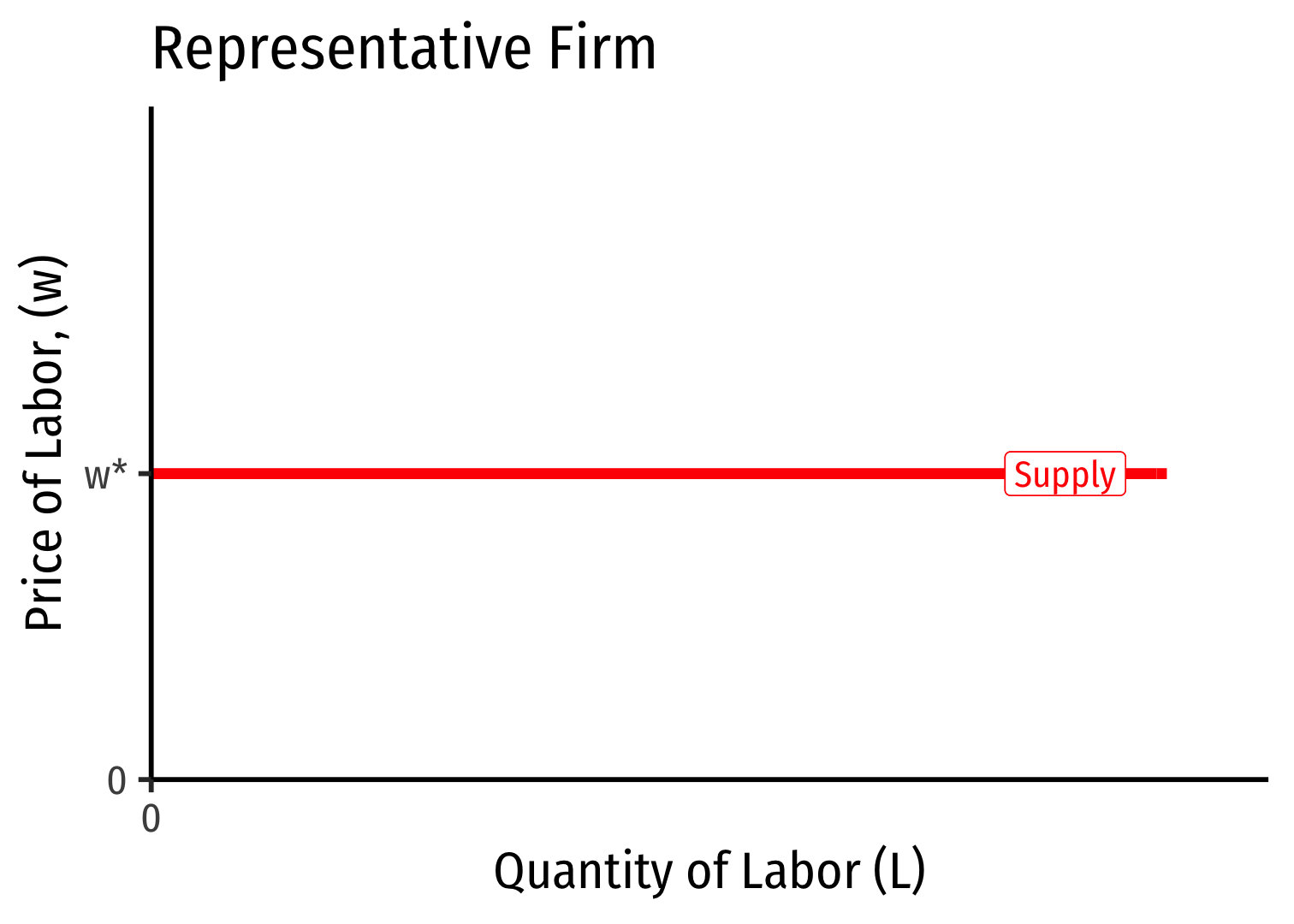

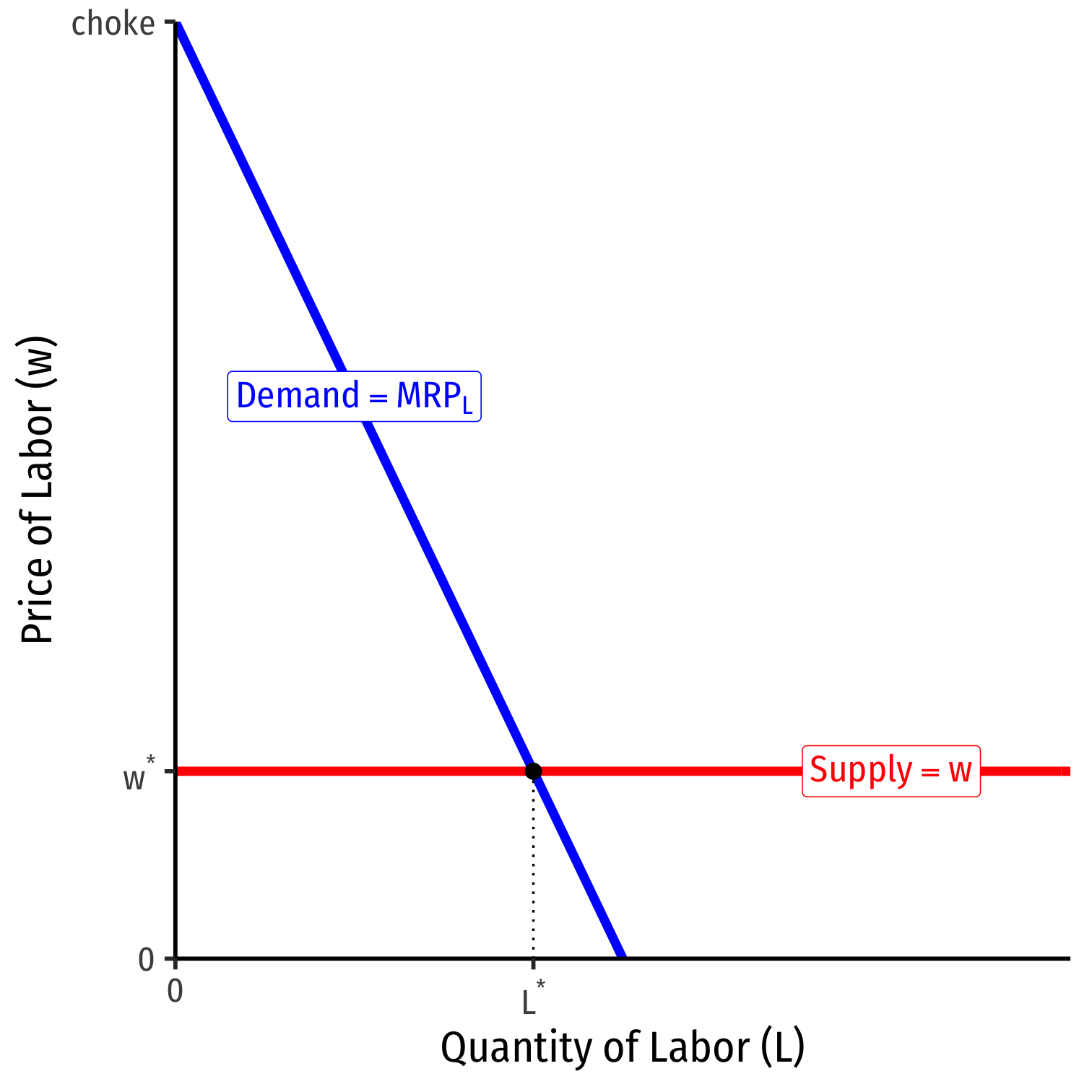

A Competitive Factor Market

- If the factor market is competitive, labor supply for an individual firm is perfectly elastic at the market wage

Labor Supply and Firm Demand

We've seen a falling MRPL, the marginal benefit of hiring labor

Marginal cost of hiring labor, w, remains constant

- so long as firm is not a big purchaser in the factor market

Labor Supply and Firm Demand

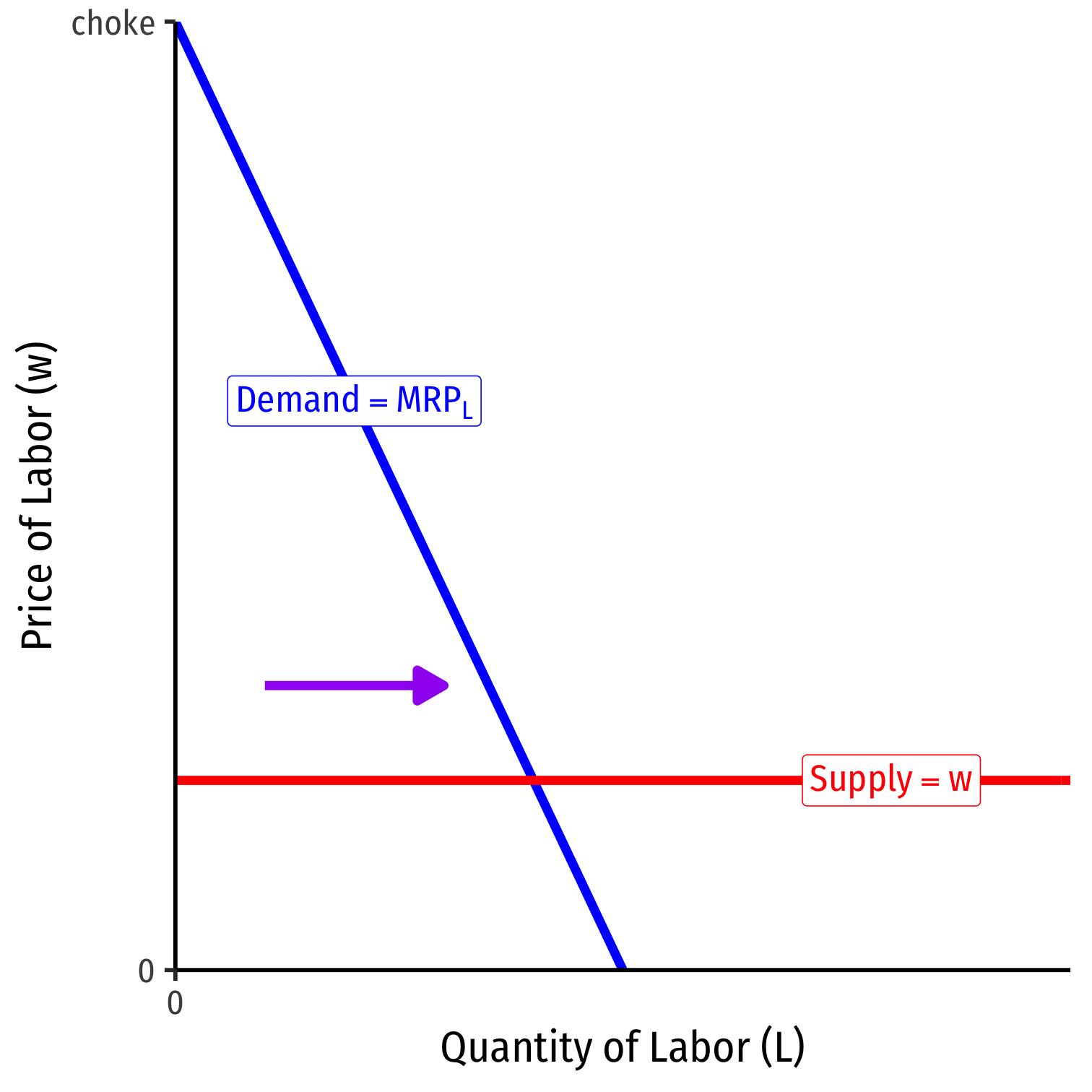

At low amounts of labor, marginal benefit (MRPL)<w marginal cost

Firm will hire more labor

Labor Supply and Firm Demand

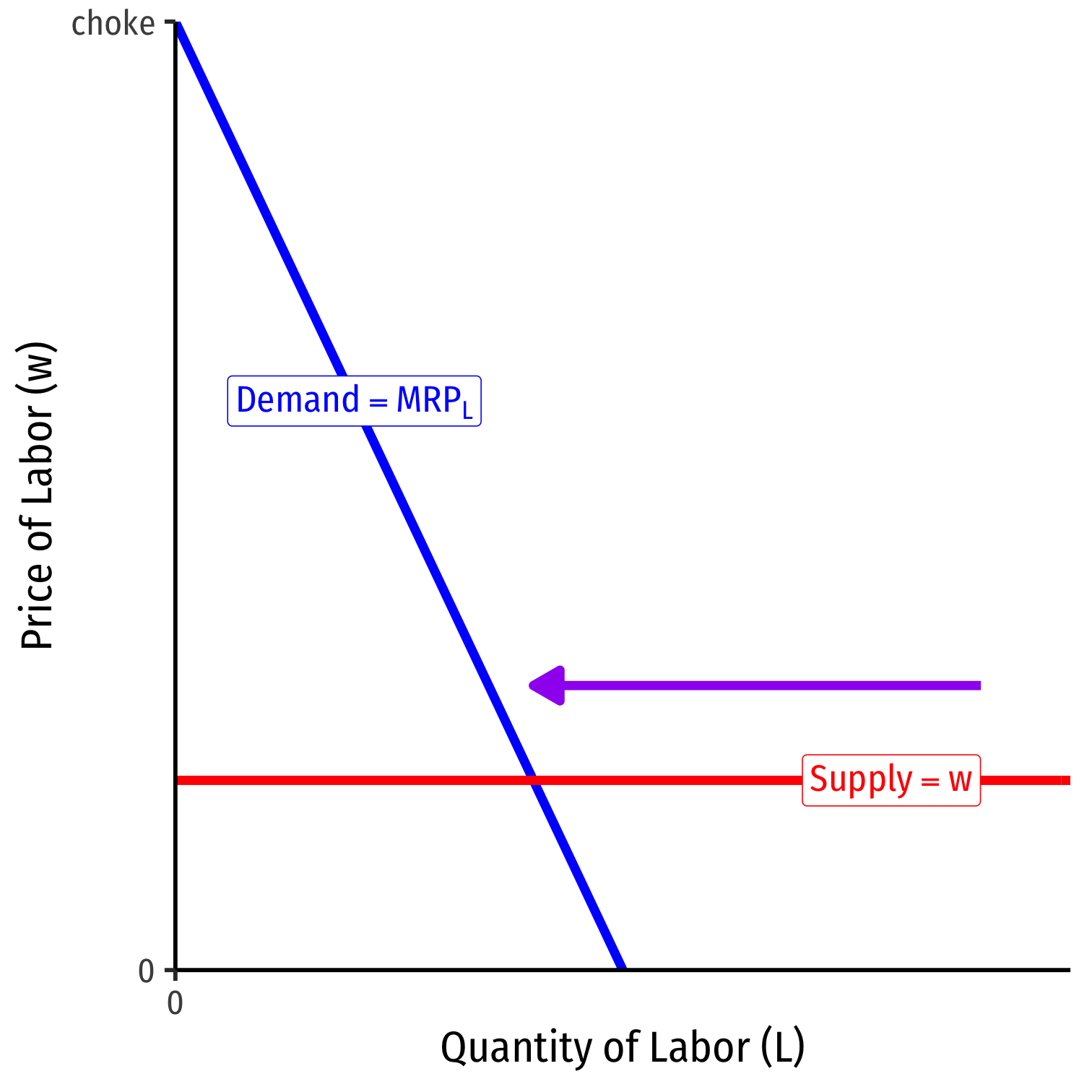

At high amounts of labor, marginal benefit (MRPL)<w marginal cost

Firm will hire less labor

Labor Supply and Firm Demand

Firm hires L∗ optimal amount of labor where w=MRPL (MB=MC)

Equivalently (rearranging): MR=wMPL

- implies that firm's producing the profit-maximizing output q∗ means firm is using the optimal amount of labor L∗

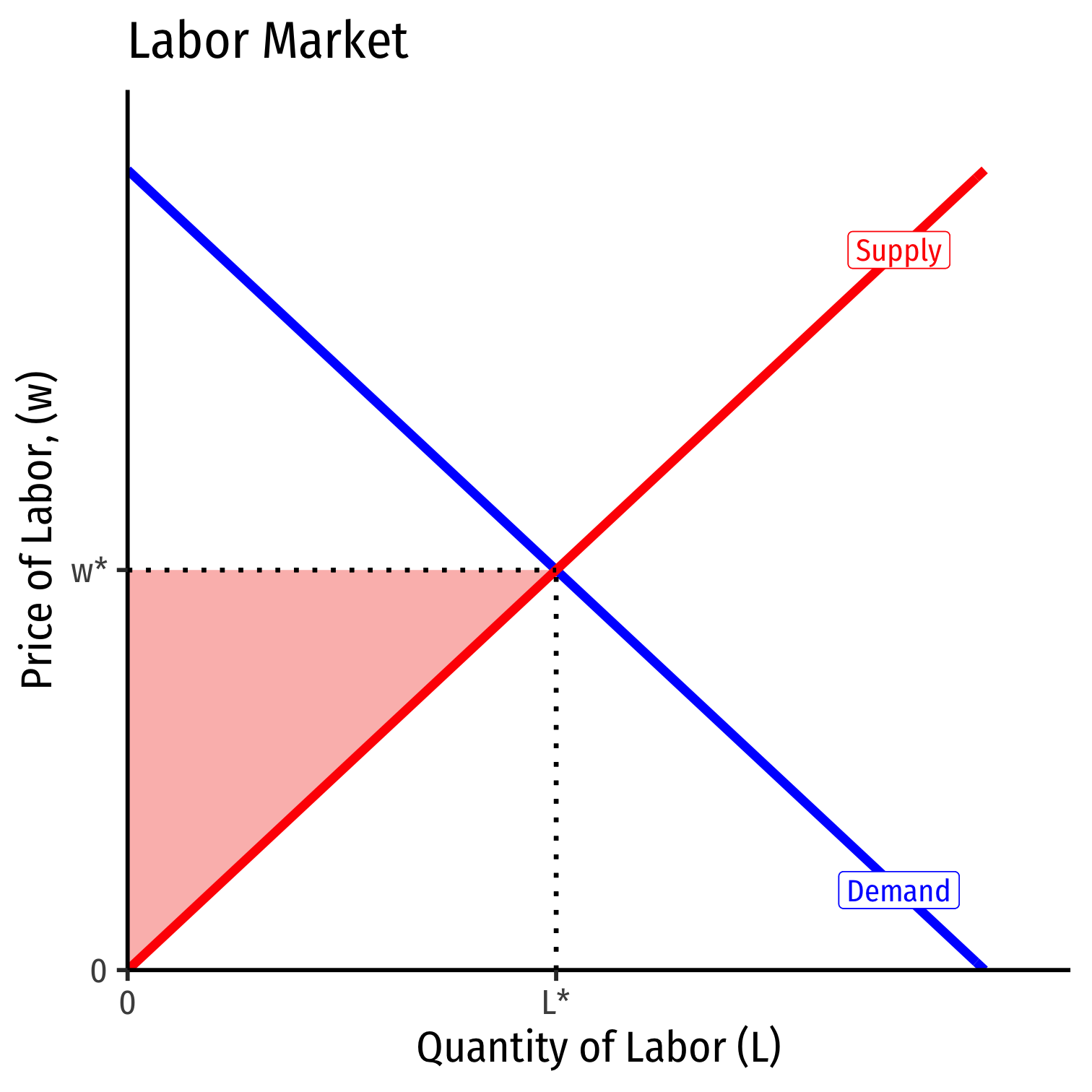

Economic Rent I

Recall supply is the minimum willingness to accept, the minimum price necessary to bring a resource to market

But all (equivalent) labor is paid the market wage, w∗ determined by market labor supply and labor demand

Some workers would have accepted a job for less than w∗

Labor earns economic rent in excess of what is needed to bring it into the market (its opportunity cost)

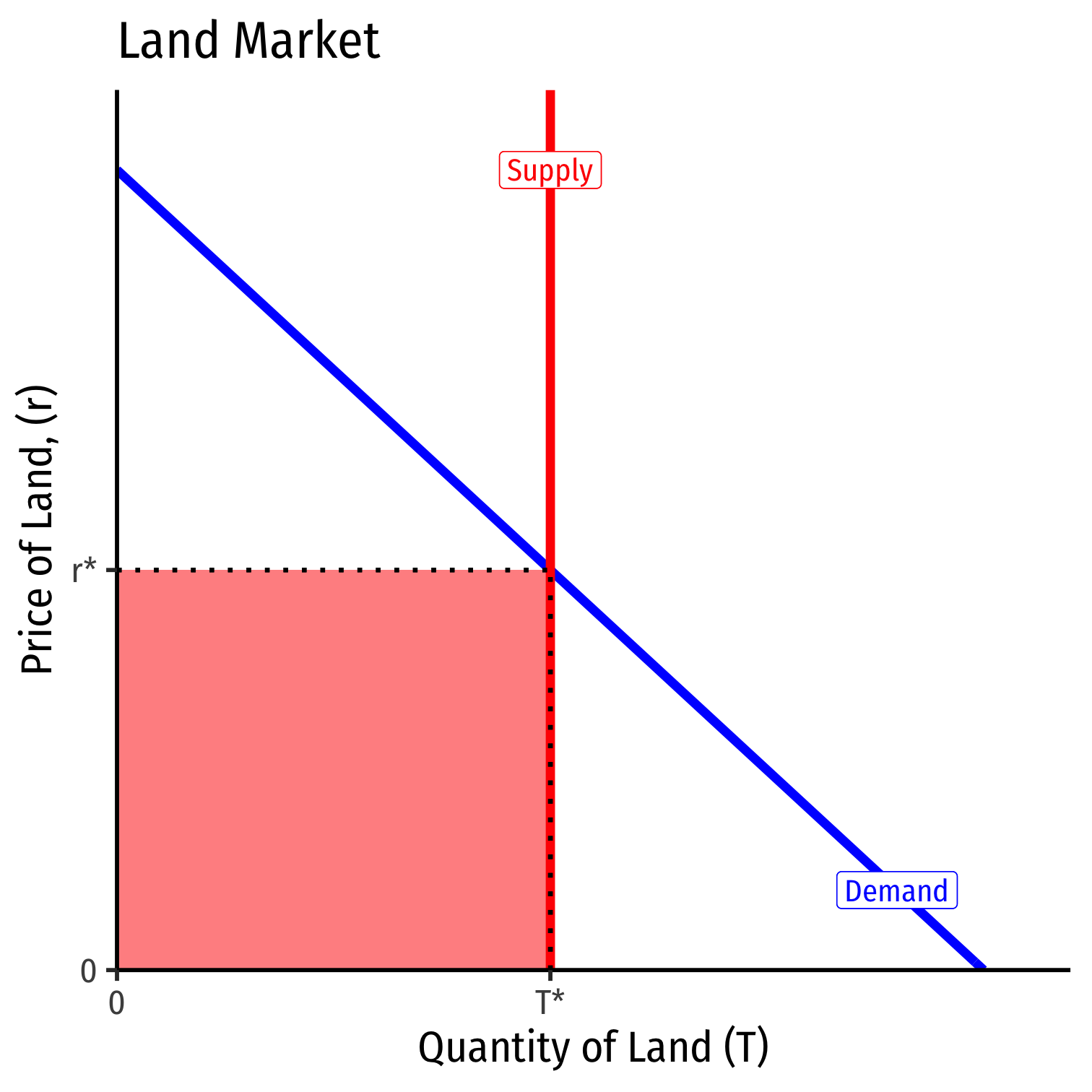

Economic Rent II

Consider a factor (such as land) for which the supply is perfectly inelastic (e.g. a fixed supply)

Then the entire value of the land is economic rent!

The less elastic the supply of a factor, the more economic rent it generates!